The big picture for Markets and the Economy in 2025

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — December 16, 2024

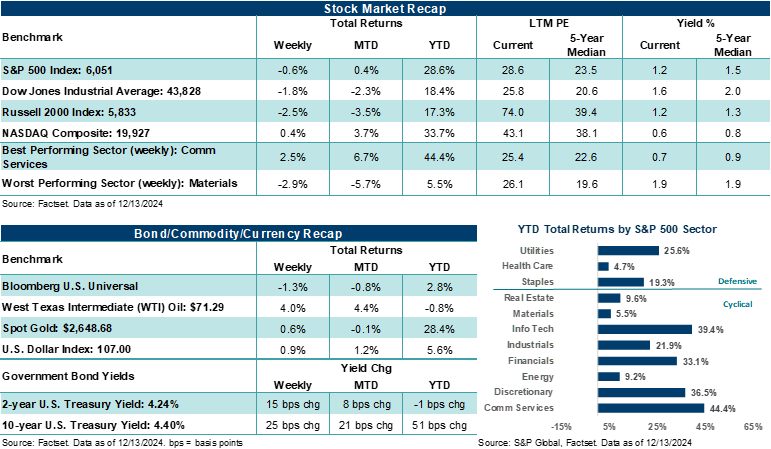

Stocks put in a mixed week of performance last week as investors digested updated inflation data and waited for this week’s final Federal Reserve policy update of the year. Stretched valuations and mixed stock momentum across Big Tech acted to complicate the market’s direction, which contributed to sending the S&P 500 Index modestly lower. That said, the NASDAQ Composite eked out a fractional gain last week, rising for the fourth straight week.

All eyes this week will be on the Federal Reserve’s policy decision on Wednesday. Market odds point to a nearly 100% chance the central bank will cut its policy rate by 25 basis points. However, it will likely be the updated Summary of Economic Projections and what Fed Chair Powell and company see for the U.S. economy and rate policy next year that moves markets.

Last week in review:

-

The S&P 500 Index closed lower by 0.6%, snapping a three-week winning streak.

- The NASDAQ Composite gained +0.4% and was the only major U.S. stock average to finish the week higher. Alphabet rose +8.6% on excitement over its quantum computing breakthrough, while NVIDIA slipped lower by 5.8% on weaker technical trading.

- Both the Dow Jones Industrials Average (-1.8%) and Russell 2000 Index (-2.5) saw sentiment cool following solid runs higher post-election.

“All eyes this week will be on the Federal Reserve’s policy decision on Wednesday. Market odds point to a nearly 100% chance the central bank will cut its policy rate by 25 basis points. However, it will likely be the updated Summary of Economic Projections and what Fed Chair Powell and company see for the U.S. economy and rate policy next year that moves markets.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

- U.S. Treasury prices were weaker across the curve, the U.S. Dollar Index strengthened, and Gold and Crude rose.

- The headline Consumer Price Index (CPI) rose +2.7% in November on an annualized basis, while the core measure (excluding food and energy) rose +3.3%. Shelter costs (which account for roughly 40% of all-items CPI) slightly decreased from October levels, while inflation across used vehicles and airfares rose less than in October. Although consumer prices came in mostly warmer-than-expected last month, we believe it is unlikely consumer prices will see a dramatic reacceleration, which should keep Fed officials on a “gradual” path of adjusting its policy rate lower in 2025. In addition, producer price inflation also came in warmer than expected in November, with the headline figure seeing its largest jump since February 2023 on an annualized basis.

- Speaking of inflation, the latest New York Federal Reserve Survey of Consumer Expectations showed inflation uncertainty rising across all time horizons. Attitudes about the labor market and household finances were mixed, with one-year ahead earnings growth expectations sitting at the top of the range going back to January 2024.

- Banks provided a mostly upbeat view of the year ahead at the Goldman Sachs Financial Services Conference. Most big banks were optimistic about their net interest income trajectory, incrementally more upbeat on capital market strength next year, and had a favorable view of the U.S. economy in 2025.

- The NFIB Small Business Optimism Index jumped to its highest level since June 2021, snapping a 34-month streak of record uncertainty. Election results signaled a major shift in the fiscal policy assessment among small business owners, with the group particularly upbeat about the potential for lower taxes and less regulation.

- Overseas, China stimulus sentiment ramped higher after Beijing said it would implement a more proactive fiscal policy approach next year, while stating monetary policy would loosen moderately. However, details were lacking. On the central bank front, the European Central Bank cut its policy rate by 25 basis points for the third consecutive meeting, as expected. Importantly, policymakers left the door open for further rate cuts in 2025. In France, President Emmanuel Macron appointed longtime ally Francois Bayrou to lead the French government and help build consensus across a deeply fractured parliament after the former PM was toppled in a no-confidence vote the previous week.

Out with the old, in with the new. The big picture for 2025.

With an eventful year winding down, U.S. stocks are on pace to record another year of strong annual returns. In fact, the S&P 500 recorded its strongest month of performance this year in November, putting the Index on pace for two consecutive years of back-to-back +25% plus returns for the first time since the late 1990s. Since the election, investors have favored small-cap stocks, Financials, Consumer Discretionary, and software companies in Tech while reducing exposure to Healthcare, Utilities, and strategies that hedge volatility. However, most recently, these trends have continued to shift and evolve as the year winds down.

As you think about the year ahead, below are a few “big picture” themes we see encompassing markets and the economy in 2025:

- Security selection makes a comeback. U.S. asset prices and valuations reflect much of what could go right over the next twelve months. A more selective investment approach may be required to help navigate a fluid environment.

- Fundamental conditions in the U.S. economy and financial markets will likely remain firm. In our base scenario, the U.S. economy should grow around its longer-term trend, core inflation should moderate to policymakers +2.0% target, and corporate earnings should grow for the fifth consecutive year. However, while asset prices could keep grinding higher in such an environment, investors should expect a more volatile backdrop next year, which could begin as soon as the first quarter.

- A second Trump presidential term offers potential benefits and risks to growth that are difficult to forecast. However, the odds favor a pro-growth outcome, in our view. Sorting through potential changes to tax policy, regulation, trade policies, and immigration might keep investors on their toes. Less regulation and the extension of expiring provisions in the 2017 Tax Cuts and Jobs Act (in addition to lowering certain taxes) could be modestly stimulative. Broad tariff implementations, however, could dampen economic growth and put upward pressure on inflation.

- Big Tech remains influential, but expanding profit growth elsewhere creates opportunities. An artificial intelligence "gold rush" has pushed the valuations of mega-cap Technology companies into rarified air. But an increasing number of industries outside of Tech could see an acceleration in profit growth and have room to rise. Investors should broaden their horizons for opportunities and selectively take advantage of potential weaknesses in Technology.

- Stick to the basics. Focus on diversification, hew exposures to the U.S., grab some yield, and be prepared for an eventful year.

Later this week the Ameriprise Investment Research Group will publish its suite of Outlook and Theme reports for 2025. The reports will highlight our views and outlook on the economy, markets, and investment strategies we believe can prepare investors for the upcoming year. Importantly, outlook reports are meant to equip investors with the big-picture items we see driving markets over the quarters ahead and provide some investment strategies to help them navigate the environment. But these are also point-in-time reports that, as time passes, become less useful as conditions change and evolve throughout the year. In our view, it’s the ongoing evaluation of our outlook throughout the year that matters most to investors, as well as our ability to identify when shifts in our guidance need to occur. Bottom line: Take some time to read through our Outlook and Theme reports before the new year. Use the reports as a solid base to build expectations for 2025, help understand the environment ahead, and even take a few tips away for helping adjust portfolios to opportunities and risks. And please use our ongoing research throughout next year (like our Weekly Market Perspectives report) to keep on top of what’s happening in the markets and economy and stay abreast of changes in our outlook as we move through what is very likely to be a year filled with ups and downs.

The week ahead:

- We expect the Fed to cut rates by 25 basis points on Wednesday and Powell to set the stage for a pause in January. We expect the Fed Chair to adopt a cautious policy tone and stress that the committee will take its time to normalize U.S. rate policy. Although Powell will be asked several times and in several different ways how changes in fiscal policies or tariffs may impact future monetary decisions, investors should expect him to keep tight-lipped on the subject and stress the committee will act appropriately as conditions change. We also wouldn’t be surprised if the committee’s updated projections for future rate policy see fewer cuts in 2025 than forecast in September.

- Preliminary looks at December manufacturing and services activity in the U.S. should show a largely steady state versus November levels. Meanwhile, November retail sales figures (excluding autos) should see a boost over October figures.

- A batch of housing data, a final look at third quarter GDP, the Fed’s preferred measure of inflation for November, and a final look at December Michigan sentiment are all on the calendar. However, outside of the Fed Meeting, the rest of this week’s releases will likely be ignored by the market as traders and professionals start to focus on the holidays and regroup for another year.

Finally, Ameriprise Weekly Market Perspectives will return for the January 6 edition. From everyone in the Ameriprise Investment Research Group, have a joyful holiday season and best wishes for a prosperous and healthy new year.