Good news is good news for investors

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — October 7, 2024

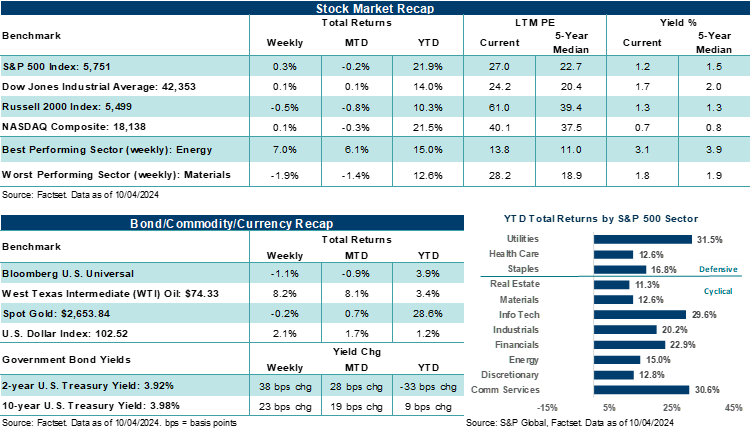

The S&P 500 Index and NASDAQ Composite each edged out their fourth straight week of gains, avoiding breaking the streak after Friday's unexpectedly strong September jobs report. A port strike on the East and Gulf Coasts that had the potential to slow economic growth in the fourth quarter quickly ended with a temporary union agreement, while violence in the Middle East continued to simmer. Also, Federal Reserve Chair Jerome Powell said if the U.S. economy evolves broadly as expected, policy rates would likely return to a neutral level over time (i.e., neither restrictive nor stimulative for growth). However, the Chair was quick to point out that policymakers are not in a hurry to lower rates, and following last week's strong jobs data, odds now heavily favor a 25-basis point rate cut in November.

Last week in review:

- The S&P 500 Index rose +0.3%. Over its four-week streak of gains, the Index is higher by +6.3%.

- The NASDAQ Composite gained +0.1%. The tech-heavy benchmark is higher by +8.7% over the last four weeks.

- Stock gains on the week were stronger across the Dow Jones Industrials Average (+0.8%) and the Russell 2000 Index (+1.5%). The Dow is up nearly +5.0% over its current four-week winning streak.

- Along with Big Tech, airlines, autos, banks, retail apparel, energy, and insurance performed well during the week.

- Government bond yields rose significantly, following stronger-than-expected labor data and falling odds of another outsized 50-basis point Fed rate cut next month. However, the 2-year/10-year Treasury spread remained positive, but barely.

- The U.S. Dollar Index strengthened against a basket of currencies.

- Gold ended slightly lower. In 2024, the precious metal is higher by over +28.0%, outperforming the S&P 500. In our view, rising U.S. debt levels, falling interest rates, a slowing U.S. economy, and an increasingly unstable geopolitical environment are key factors that could remain supportive for the noble metal over the next six to twelve months.

- West Texas Intermediate (WTI) crude settled higher, logging its best week since March 2023. Crude prices have jumped higher recently on growing anxiety that the current Middle East conflict across Israel, Gaza, Lebanon, and Iran continues to escalate to levels that may start to risk global crude supply. Roughly 20% of the world's oil supply runs through the Strait of Hormuz.

- Here at home, the International Longshoremen's Association agreed to suspend their strike until January 15th, which will allow cargo to move again off the East and Gulf Coast ports. A tentative agreement boosts dock worker pay by about +62% over six years and gives time for negotiations to develop on other key issues, such as automation. Bottom line: A port strike that could have slowed growth and disrupted the economy and markets for a period in the fourth quarter has been avoided. Notably, it's one less concern investors need to contend with through yearend.

- September nonfarm payrolls grew by an unexpectedly strong +254,000, while the unemployment rate edged lower to 4.1% last month from 4.2% in August. Further, July and August job figures were revised higher by a combined +72,000. Add in a very healthy level of available jobs in the U.S. (over +8 million in August) and a strong September private payrolls report, and you have a U.S. economy that continues to benefit from a labor market on firm footing.

- Finally, ISM manufacturing showed activity coming in slightly below consensus for September, while ISM services activity beat estimates and saw its highest level since February 2023.

“We believe investors should maintain a somewhat optimistic view of the U.S. economy and financial markets heading into yearend. Investing in opportunities across cyclical areas inside/outside of Technology, putting excess cash back to work in the market during potential periods of market stress, and locking in higher interest rates across bond allocations are strategies that could help investors navigate the final months of the year.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

Reasons to maintain a positive but balanced outlook as the year winds down.

As it stands at the moment, we believe the bulls appear to have the edge in directing stock traffic at the start of the fourth quarter. Economic data remains solid, particularly on employment, and the Fed easing cycle is in its early stages. Notably, last week's falling odds for an outsized 50-basis point cut in November and increasing odds for a more gradual 25-basis point cut next month should be music to investor's ears. A Fed that can gradually bring down its policy rate in an environment where growth remains positive and inflation continues to ebb lower is likely far more supportive for asset prices than an environment in which the Fed has to lower rates quickly and by outsized cuts (i.e., 50-basis point increments).

Simply, good news is good news at the moment. Economic growth should remain firm (we see the U.S. economy growing by +2.5% in Q3 and by +1.9% in Q4), inflation should continue to ebb lower, labor conditions remain solid, and rate pressures should ease, causing less stress on consumers and businesses over time. The potential for a lingering port strike in the U.S. has been avoided. China is adding stimulus to the world's number two economy. Most global developed central banks are also in the process of easing policy rates. And, by the way, NVIDIA's CEO Jenson Huang said last week that the demand for its new artificial intelligence chip Blackwell is "insane." In our view, the fundamental backdrop for asset prices remains supportive, and investors should take note of it.

That said, valuations across major U.S. averages, such as the S&P 500 and NASDAQ, are elevated, and much of the "soft-landing" narrative described above has been priced into stocks, in our view. How much better or worse data comes in around expectations, particularly as the Q3 earnings season ramps up, could be a key factor in driving asset prices in Q4.

In addition, Middle East tensions continue to ratchet higher, which exposes the market to elevated "event shock" risk. For example, an unexpected and sudden spike in oil prices (potentially caused by supply disruptions in the Middle East) could suddenly slow global economic growth more than expected, causing corporate profits to fall, which then leads to lower stock prices as profit forecasts for the future decline. While this type of geopolitical event can't really be planned for and seldom is discounted into stock prices prior to occurring, it's a risk investors should understand, given U.S. stocks sit near all-time highs.

In addition, potential volatility after the U.S. election is another wildcard factor that should temper investor bullishness. Assets are priced for divided government, and while the odds are low the November U.S. election produces a one-party control result in Washington, we believe the potential for stock volatility post-result shouldn't be discounted to zero.

In sum, we believe investors should maintain a somewhat optimistic view of the U.S. economy and financial markets heading into yearend. Investing in opportunities across cyclical areas inside/outside of Technology, putting excess cash back to work in the market during potential periods of market stress, and locking in higher interest rates across bond allocations are strategies that could help investors navigate the final months of the year.

The week ahead:

The third quarter earnings season will kick off this week with PepsiCo, Delta Airlines, and some of the big banks reporting results. Consumer and producer inflation updates, as well as fresh looks at consumer sentiment, line the economic calendar.

- Q3'24 S&P 500 earnings per share (EPS) is expected to grow by +4.2% year-over-year on revenue growth of +4.7%. S&P 500 EPS expectations have moved down for the current quarter, leaving a lower hurdle rate for companies in aggregate to surpass over the coming weeks. Information Technology is again expected to provide a large tailwind to S&P 500 profits in the third quarter, while Energy is expected to be the largest drag. Health Care and Communication Services should also be additive to S&P 500 profit growth. Investors will likely focus on artificial intelligence trends, with "return on investment" playing a growing theme in how Big Tech results are interpreted in the market. Impacts/outlooks from Fed easing, updates on bifurcated consumer trends, the health of business spending, operational cost management/efficiency, labor trends, and profit margins will also help shape how the market reacts to Q3 earnings.

Consumer and producer inflation is expected to have cooled slightly in September on most major measures, while a preliminary look at October Michigan consumer sentiment is expected to show a slight uptick. The September FOMC meeting minutes, weekly jobless claims, and a fresh look at small business sentiment will also provide key updates on the direction of policy and economic sentiment.