Happy 2nd birthday to the bull market

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — October 14, 2024

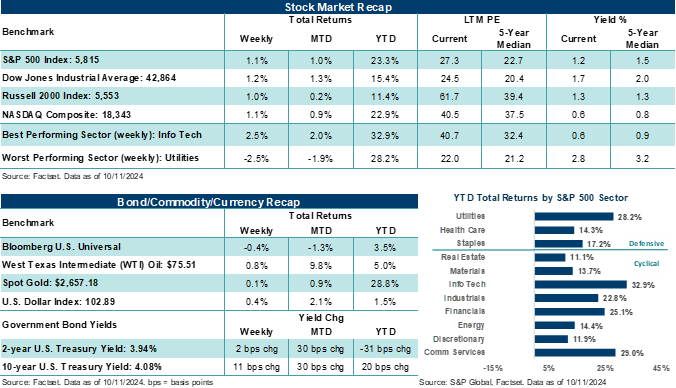

Stocks continued to grind higher last week, with the S&P 500 Index finishing above 5,800 for the first time on Friday. The NASDAQ Composite ended the week less than 2.0% away from its July high. Mixed economic releases and the Federal Reserve’s minutes from the September meeting kept a rate cut firmly on the table for November, while the kickoff of bank earnings mostly impressed.

Last week in review:

- The S&P 500 and NASDAQ finished their fifth straight week higher, rising by +1.1% each.

- The Dow Jones Industrials Average and Russell 2000 Index each rose by roughly +1.0%.

- Banks were also stronger, with JPMorgan Chase and Wells Fargo reporting third-quarter results to help start the earnings season. For example, JPMorgan comfortably surpassed third-quarter profit estimates. At the same time, investors lifted bank shares post-report on Friday as expectations for positive credit trends and improving investment banking/trading/loan activity out into 2025 across the group pushed sentiment higher.

- However, reports from PepsiCo, Domino’s Pizza, and Delta Airlines during the week were less impressive, as consumers continued to become more price-sensitive following years of price hikes. Delta noted that the CrowdStrike outage cost the airline $380 million in revenue in the prior quarter while lowering profit guidance for the current quarter.

- Elsewhere, a preliminary look at October Michigan consumer sentiment came in below estimates, while Hurricane Milton unleashed more damage across swaths of Florida, closely following Hurricane Helene. Insured damages from Milton could range between $40 billion and $50 billion, less than originally feared, but on top of Helene’s estimated insured losses of $10 billion. Weekly jobless claims rose more than expected, though ongoing Boeing strikes, and Hurricane Milton may have played a role.

- U.S. Treasury yields ticked slightly higher, with 2-year and 10-year yields finishing around 4.00%.

- West Texas Intermediate (WTI) crude finished higher for the fourth week out of five, while Gold ended the week up.

- The U.S. Dollar Index ended higher, breaking a nine-day winning streak on Friday.

“At least based on history and these simple averages, there may still be more life in this bull. That said, there are several instances across history where a bull market has lasted far longer than the average and died much earlier. Yet, the frameup adds some perspective around the strength and duration of the current bull market, which helps ease some concerns that what we have seen over the last two years is out of the ordinary. At least thus far, this bull market run has looked run-of-the-mill, in our view.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

The bull market turns two years old

The current bull market turned two years old over the weekend, helping remind investors that markets can climb higher even when the path forward for inflation, interest rates, growth, and profits isn't always clear.

Since bottoming on October 12th, 2022, the S&P 500 Index has climbed higher by over +62% cumulatively through last Friday. Take a moment to think back to the macroeconomic environment on October 12th, 2022. The S&P 500 was lower by nearly 25% for the year, the headline Consumer Price Index (CPI) stood at an eyepopping +8.2% year-over-year at the end of September, and the Federal Reserve was knee-deep in aggressively raising its policy rate by large increments each meeting in an effort to combat near record-high inflation pressures across the economy. At the time, the U.S. economy had shown it had contracted in both the first and second quarters of the year.

The combination of these pretty bleak factors had many investors on recession watch and fearing stocks and bonds could fall even further. However, October 12th, 2022 (a period defined by elevated uncertainty, market stress, economic weakness, high inflation, and rapidly increasing interest rates) marked the bottom of the last bear market and the turning point for stocks. As a side note, artificial intelligence made its first mainstream introduction to the world in November 2022 through ChatGPT. Since the end of October 2022, the S&P 500 Information Technology Index is higher by +100% cumulatively, something few may have believed would be possible at the time given the tech index was down over 33% year-to-date on October 12th, 2022.

While the broader stock market hasn't necessarily moved in a straight line over the last two years, stocks have ground higher since bottoming in October 2022 despite numerous challenges, uncertainties, and reasons to be fearful of what lies ahead.

Notably, the over +62% return in the S&P 500 over the last two years isn’t that aggressive by historical standards when looking at overall bull market runs. In fact, going back to 1929, the S&P 500 has averaged a +114.4% gain during a full bull market run, with the duration of the run lasting 1,011 days on average, according to Bespoke Investment Group. Bull markets tend to be long and steady, while bear markets have a history of being short and fierce.

At least based on history and these simple averages, there may still be more life in this bull. That said, there are several instances across history where a bull market has lasted far longer than the average and died much earlier. Yet, the frameup adds some perspective around the strength and duration of the current bull market, which helps ease some concerns that what we have seen over the last two years is out of the ordinary. At least thus far, this bull market run has looked run-of-the-mill, in our view.

Looking ahead, stocks will likely move on incoming data around employment, inflation, and corporate earnings, which should remain favorable for stock prices through year-end. Over the very near-term third-quarter earnings reports, the upcoming U.S. election and tensions in the Middle East have the potential to create periods of brief volatility in the fourth quarter. But as long as fundamental conditions remain firm, the bull market should continue to ride the near-term ups and downs in sentiment while continuing its grind higher. Notably, bull markets don't die of old age. Bull markets usually end because of a large event shock or policymakers' "need" to slow the economy with higher interest rates, which can sometimes cause a recession.

At least over the intermediate term, these two conditions appear less likely. Importantly, we should celebrate the fact that in all the uncertainty investors have had to endure over the last few years, stocks did what they always do — look ahead. Before it was obvious growth would hold, inflation would ebb lower, policy rates would start to come down, and corporate profits would rebound, stocks started and continued to climb higher. Investors can generally ride these shifts by avoiding the temptation to bail on stocks during difficult periods and having a strategy in place to maintain proper exposure in all market environments. Hence, it's easier to stay the course when the unexpected pops up, which always does, eventually.

The week ahead:

- Corporate earnings will come into focus this week, with 43 S&P 500 companies scheduled to report third quarter results. Updates on where consumers are spending on goods as well as fresh looks at home data line the calendar.

- Financial heavyweights such as Bank of America, Goldman Sachs Group, Morgan Stanley, and Citigroup will all report third quarter results this week. In addition, Johnson & Johnson, Walgreens Boots Alliance, UnitedHealth Group, Netflix, and United Airlines will also provide updated looks into some of the business trends/outlooks for industries outside Financials.

- Notably, analyst profit estimates for the fourth quarter and first half of 2025 have started to ease from elevated levels over recent weeks, allowing more opportunity for companies to achieve and possibly surpass estimates in the future. In our view, corporate profit growth that remains positive over the coming quarters but is in tune with normalizing economic activity could provide a tailwind for stock prices.

- Retail sales in September are expected to remain healthy across a broad set of categories, while September building permits and housing starts are expected to decline versus August levels.