What could happen to markets after election day?

ANTHONY SAGLIMBENE – CHIEF MARKET STRATEGIST, AMERIPRISE FINANCIAL

WEEKLY MARKET PERSPECTIVES — October 28, 2024

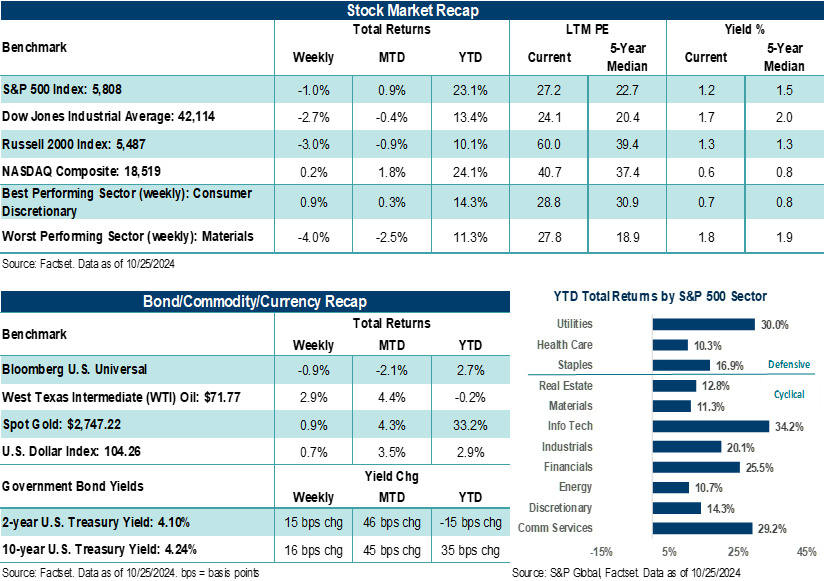

Stocks finished mostly lower last week, with the S&P 500 Index snapping a six-week winning streak. However, the NASDAQ Composite was able to finish the week higher, hitting a new all-time intraday high on Friday and surpassing its previous July record intraday top. Third quarter earnings reports came in mostly positive during the week, with 75% of S&P 500 companies reporting results thus far exceeding analyst estimates.

Last week in review:

- The S&P 500 slipped 1.0%, while the Dow Jones Industrials Average and Russell 2000 Index lost 2.7% and 3.0%, respectively.

- The NASDAQ Composite bucked the trend, gaining +0.2%. Big Tech was mostly firmer on the week, with Tesla jumping +22.0% on stronger-than-expected earnings and CEO Elon Musk saying vehicle sales could grow by +30.0% over the next year.

- That said, cautious corporate commentary out of Apple, Starbucks, and Qualcomm, for example, pointed to forming cracks in the consumer resiliency theme. McDonald's stock fell after reporting an E. coli outbreak linked to its Quarter Pounder hamburgers, and Boeing failed to reach an agreement with its striking labor union.

“The U.S. economy and stock market are likely to grow over time regardless of the composition of Washington, meaning emotional responses to the election that draw one away from a well-constructed investment strategy is a recipe for derailing investment success. Our advice around this election: Stay the course.”

Anthony Saglimbene - Chief Market Strategist, Ameriprise Financial

- With roughly 37% of S&P 500 third quarter reports complete, blended earnings per share (EPS) growth is higher by +3.6% year-over-year on revenue growth of +4.9%. The Index is on pace for its fifth straight quarter of positive year-over-year earnings growth.

- September manufacturing and services activity beat expectations, weekly initial jobless claims fell (though continuing claims rose to their highest level in nearly three years), and September home sales rose month-over-month — rising to their highest level since May 2023.

- Durable goods orders fell in September, though beat expectations. However, ex-transportation durable orders were up month-over-month. Final October Michigan Consumer Sentiment was revised slightly higher, with one-year ahead inflation expectations ticking down to 2.7% from 2.9% in the preliminary reading.

- U.S. Treasury prices were weaker across the curve as yields moved higher. The U.S. Dollar Index moved higher, Gold hit another fresh all-time high, and West Texas Intermediate (WTI) crude rose nearly 3.0%.

- Early Saturday, Israel launched a retaliatory attack on Iran's missile manufacturing facilities and surface-to-air missile defense sites in response to the 180 missiles Iran fired at Israel on October 1st. Elevated tension in the Middle East continues to be a source of geopolitical instability and a wildcard factor for market volatility.

What could happen after election day?

With the U.S. election now just days away, it's crunch time for presidential candidates and down-ballot participants to make their final cases to the shrinking number of undecided Americans that will likely determine races across the country. More importantly, it's time for candidates to turn up their ground games to get voters to the polls if they haven't already voted. From a market perspective, stock volatility has inched modestly higher since the end of September (but well within historical norms) as investors have attempted to discount potential election results. Granted, that modest shift higher in volatility has been largely accompanied by rising stock prices. Yet, investors should keep the following considerations in mind as we all navigate through the final run-up to election night in America and post-election outcomes.

Markets may already be leaning toward a Trump win. Although the polls are extremely tight, and it's anyone's race to win, the stock and bond markets have shown recent momentum that appears to favor a result that puts former President Trump back in the White House. Government bond yields have risen, the U.S. dollar has strengthened, and areas of the stock market that would benefit from less regulation and lower taxes have ground higher. Some of this is related to a strong economy and growing profits, while some of this momentum may be attributed to investors increasingly discounting a Trump victory.

Off to the races or sell the news? In our view, the market can perform well through year-end whether Vice President Harris or former President Trump wins in November. We believe fundamental conditions in the U.S. are solid, seasonality factors/historical trends are favorable for stocks, and known election results, which let investors finally move on from the election, could see major equity averages press higher into the end of the year. However, a Trump win could also see some temporary market volatility due to the increased potential for additional tariffs and, depending on the makeup of Congress, open the door for increased debt and deficit spending that would have to be weighed against potential benefits from lower taxes/ regulations. In addition, a Harris victory could see the stock market roll back some of the positive momentum of recent weeks, as the potential for higher taxes and additional regulations temporarily reset investor expectations. Notably, checked power from Congress could limit market reactions regardless of the presidential outcome.

Odds continue to favor a divided government post-election. However, one-party control in Washington could lead to a post-election sell-off. From an odds standpoint, a Trump victory in November carries with it a chance for Republicans to retain the House of Representatives and recapture the Senate. Simply, a win for Trump would likely represent a shift away from the policy of the current administration and could filter through into down-ballot contests that help Republicans establish one-party control in Washington. Given the tariff proposals made by the former President, this result may be viewed as inflationary, which could see longer-term government bond yields rise post-election and stock market reactions border on positive (i.e., lower taxes/regulation) to negative (the potential for higher debt and deficit spending in future years). A Democratic sweep carries the least likely odds, in our view. Still, it would potentially come with a more negative market reaction, as debt/deficit spending likely increases (though probably not as much under Republican control) but is accompanied by higher taxes and more regulation. Bottom line: Investors should cheer an outcome that leads to the continuation of a divided government based on what we believe are pretty poor economic policies from both camps.

A contested presidential election result that drags on for weeks would likely be a market negative temporarily. However, we would look through the dislocation and put excess cash to work in stocks and bonds. An election result that is clear, decisive, and known relatively quickly (e.g., within a couple of days) is the best-case scenario for markets, in our view. Whether America actually gets such an outcome is highly debatable at the moment. For example, in 2000, the Gore/Bush presidential match-up saw the S&P 500 Index fall roughly 8.0% between election day and the end of the year, as a final decision on who would sit in the White House remained undetermined following the election. The presidential contest lingered on over a month after election day and had to be decided by the Supreme Court. While stocks fell, bond and gold prices rose as investors sought safety and diversification in a period of market stress and uncertainty. While we don't anticipate such an event this time around, the race is tight, and a few battleground states could see the presidential winner take the state in the electoral college by just a few thousand votes. Bottom line: Regardless of whether the presidential winner is known rather quickly, a result takes time, or legal battles develop that prolong the outcome, the next President of the United States will take the oath of office on January 20th, 2025, at noon EST. Any volatility that develops based on near-term election unknowns or contested legal battles is a buying opportunity for investors that have excess cash to place in stocks and bonds, in our view.

Most importantly, don't let your emotions get the best of you following the election, and don't make rash investment decisions. Americans will get through this election, just like they have for almost 250 years. If your candidate wins in November — congratulations. If your candidate lost — bummer. Honestly, who sits in the White House or which party controls Congress is less consequential to the economy and markets than most may believe. As we've noted in previous commentaries, your portfolio doesn't care who wins in November. The U.S. economy has grown under every single administration and combination of Congress, going all the way back to President Eisenhower. The S&P 500 Index has only fallen under Richard Nixon and George W. Bush's administrations, largely due to an inflation shock and the Great Financial Crisis. In fact, the S&P 500 has only fallen in seventeen years, going all the way back to 1945. Bottom line: The U.S. economy and stock market are likely to grow over time regardless of the composition of Washington, meaning emotional responses to the election that draw one away from a well-constructed investment strategy is a recipe for derailing investment success. Our advice around this election: Stay the course.

The week ahead:

The final full week of election campaigning, Big Tech earnings, updated looks at growth/inflation, and key employment reports will all vie for investors' attention this week.

- Presidential candidates and their surrogates will crisscross the country in the final run-up to Election Night in America on November 5th.

- Alphabet and AMD report their profit results for the previous quarter on Tuesday. Meta Platforms and Microsoft will follow on Wednesday, with Apple, Amazon, and Intel rounding out the week's Big Tech reports on Thursday. While the Magnificent Seven could see double-digit profit growth over the next five quarters, so too could the rest of the market. This means that, if analysts are correct, the broadening of profit growth among more sectors and companies next year could help reduce the disparity between Big Tech/Mag Seven and the rest of the market.

- Updates on job openings (Tuesday), a first look at Q3 GDP (Wednesday), the Federal Reserve's preferred inflation measure (Thursday), and the all-important nonfarm payrolls report for October (Friday) will keep investors very busy.