Can you borrow against your 401(k) plan before you retire?

Borrowing or withdrawing funds from your 401(k) before retirement is a big decision. After all, you’ve worked hard and saved hard to build up your retirement fund.

Most people have two options:

Whether you’re considering taking out a loan against your 401(k) vs. a withdrawal, an Ameriprise financial advisor can help you make an informed decision that considers the long-term impacts on your financial goals and retirement.

Here are some common questions and concerns about borrowing or withdrawing funds from your 401(k) before retirement.

A 401(k) loan

A 401(k) loan allows you to take out a loan against your own 401(k) retirement account, or essentially borrow money from yourself. While you’ll pay interest similar to a more traditional loan, the interest payments go back into your account, so you’ll be paying interest to yourself.

You can borrow against your 401(k) for a variety of reasons, such as funding the purchase of a house or paying for a dependent’s college tuition. While there are some plans that only allow participants to take a loan for certain approved reasons, in most cases, you won’t need to declare why you are borrowing against your 401(k).

Common 401(k) loan questions:

Can I take out a loan against my 401(k)?

Check with your plan administrator to find out if 401(k) loans are allowed under your employer’s plan rules. Keep in mind that even though you’re borrowing your own retirement money, there are certain rules you must follow to avoid penalties and taxes.

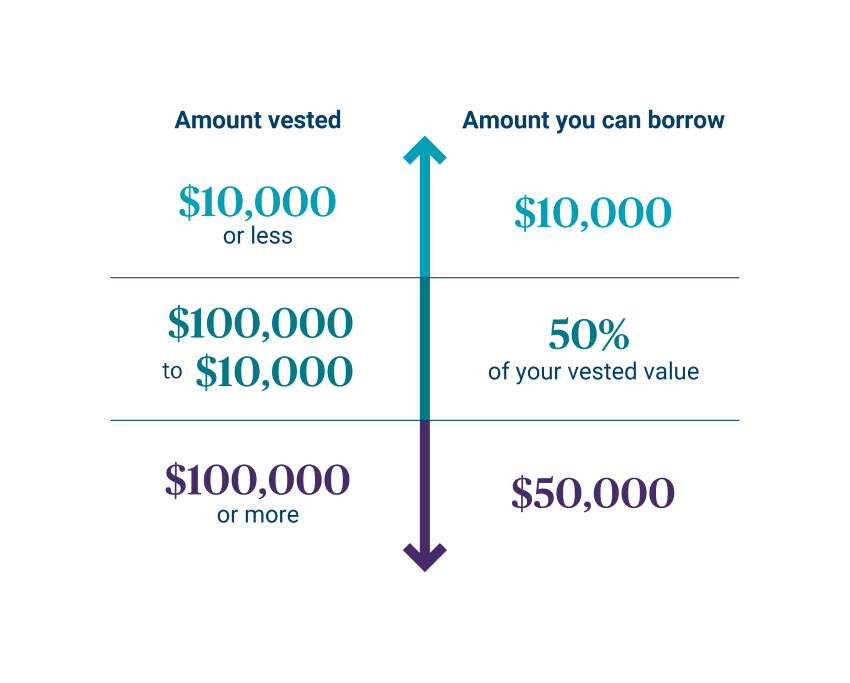

How much can I borrow against my 401(k)?

You can borrow up to 50% of the vested value of your account, up to a maximum of $50,000 for individuals with $100,000 or more vested. If your account balance is less than $10,000, you will only be allowed to borrow up to $10,000.

How often can I borrow from my 401(k)?

Most employer 401(k) plans will only allow one loan at a time, and you must repay that loan before you can take out another one. Even if your 401(k) plan does allow multiple loans, the maximum loan allowances, noted above, still apply.

What are the rules for repaying my 401(k) loan?

In order to be compliant with the 401(k) loan repayment rules, you’ll need to make regularly scheduled payments that include both principal and interest, and you must repay the loan within five years. If you’re using your 401(k) loan to buy a primary residence for yourself, you may be able to extend the repayment period.

What if I lose my job before I finish repaying the loan?

If you leave or are terminated from your job before you’ve finished repaying the loan, you typically have 60 days to repay the outstanding loan amount.

What happens if I don’t comply with the 401(k) loan repayment rules?

Failure to follow the 401(k) loan repayment rules may result in tax penalties in addition to a 10% early withdrawal penalty.

Summary of loan allowances

Pros and cons of taking loans against your 401(k)

| Advantages of a 401(k) loan | Disadvantages of a 401(k) loan |

|---|---|

| Taking a loan against your 401(k) is generally a quick, easy process | Money removed from your 401(k) will not be able to grow and will not benefit from the effects of compound interest |

| If you follow the 401(k) loan repayment rules, you won't be subject to taxes or penalties the loan amount | If you don't follow the 401(k) loan repayment rules, you may be subject to taxes and penalties |

| You don't need a credit check for a 401(k) loan, and your credit won't take a hit if you default | If you lose (or leave) your job while the loan is outstanding, you typically will have to repay your 401(k) loan within 60 days |

| Interest paid on the loan is not lost to a lender, because you are the lender | You must replace the money you borrowed from your 401(k) with post-tax dollars |

| There are no early repayment penalties if you pay off the loan early | You can't deduct loan interest payments for tax purposes |

Withdrawals from a 401(k)

401(k) hardship withdrawals

If you find yourself facing dire financial concerns and need cash urgently, your 401(k) plan may offer a hardship withdrawal option. Unlike borrowing against your 401(k), you won’t have to repay the money you take out, but you will owe taxes and potentially a premature distribution penalty on the amount that you withdraw. In addition, IRS 401(k) hardship withdrawal rules state that you may not take out more money than what is needed to cover your hardship situation.

In order to qualify for a 401(k) hardship withdrawal, your plan administrator must offer this option (not all of them do) and you must be facing an “immediate and heavy financial need.” Approved 401(k) hardship withdrawal reasons include:

- Postsecondary tuition for you or your family

- Medical or funeral expenses for you or your family

- Certain costs related to buying, or repairing damage to, your primary residence

- Preventing your immediate eviction from or foreclosure of your primary residence

If you experience a financial hardship from a circumstance not on this list, you may still be able to qualify for a hardship withdrawal, so check with your plan administrator.

In-service, non-hardship withdrawals

This type of withdrawal is only allowed under certain plans and is mainly used by those who would like to explore other investment options. Learn more about in-service distributions. An Ameriprise financial advisor can provide more detailed information on in-service 401(k) distributions.

Pros and cons of withdrawing funds from your 401(k)

| Pros | Cons |

|---|---|

| You'll get access to cash quickly | You'll be taxed on the amount that you take out |

| If you're under 59.5 years of age, you'll be subject to a 10% 401(k) withdrawal penalty | |

| It may affect your long-term retirement savings goals |

Withdrawing vs cashing out your 401(k)

Withdrawing money from your 401(k) is not the same thing as cashing out. You can do a 401(k) withdrawal while you’re still employed at the company that sponsors your 401(k), but you can only cash out your 401(k) from previous employers. Learn what to do with your 401(k) after changing jobs.

401(k) loan vs. withdrawal

Taking money out of your 401(k) plan is a big decision that can impact your savings progress and long-term retirement goals. If you’re contemplating withdrawing from your 401(k) vs. taking out a loan, consider connecting with an Ameriprise financial advisor. They’ll work with you to carefully weigh the risks, costs and benefits.

Rollover evaluator

If you have multiple retirement savings accounts held in more than one place, the rollover evaluator will help educate you to understand the pros and cons of keeping your retirement savings in an employer-sponsored plan such as a 401(k) or 403(b) versus rolling it over into an IRA.

RELATED INFORMATION

Feel more confident about reaching your retirement savings goals with an Ameriprise advisor.

Or, request an appointment online to speak with an advisor.

Background and qualification information is available at FINRA's BrokerCheck website.